In recent years there has been a significant increase in the number of people who have decided to rent out their home and become a first time landlord. Negative equity has left many in the position where they cannot afford to sell their home, yet due to changing life circumstances, their home is no longer suitable. One common example is young families who have outgrown an apartment and need to move to a larger family home. This has led many to renting out their own home whilst moving into a rental property themselves.

If you are considering becoming a first time landlord, below are some of the important things that you need to know. Many of these are particularly important in the context of assessing the costs involved in renting out your home and becoming a landlord.

1. You must complete an annual tax return

If you expect to have rental profits of greater than €3,174 per annum, you are considered to be a “chargeable person” and must register for income tax from the date that the property is first let. You can do this using a TR1 form available from the Revenue website www.revenue.ie.

If you will not have rental profits of greater than €3,174 you are not a “chargeable person” and are not required to register for income tax. Instead you must complete a Form 12 annually.

You must prepare an income tax return every year even if you think you do not have a tax liability. In most cases you will require assistance from an accountant or tax consultant to do this. This represents an extra cost but is tax deductible. A good accountant or tax consultant should also save you tax or ensure you avoid any accidental errors or non compliance through their advice.

2. You will be likely to have a tax liability

You will be subject to PAYE and USC on your rental “profits”. Remember that profits for tax purposes are different to what you might personally consider your profit (or lack thereof) to be. Just because the rents you receive may not cover your mortgage repayment, this doesn’t mean you don’t have a tax liability. Unfortunately many first time landlords do not realise this and a substantial tax bill can come as a very nasty surprise.

The reason that you may still have a tax bill even if the rents received do not cover the mortgage repayment is that your full mortgage repayment is not a tax deductible expense. Normally only 75% of the interest portion of a mortgage repayment is allowed as a tax deduction against the rents received. (Note that 100% of mortgage interest relief is available since 1 January 2016 to landlords meeting certain conditions relating to tenants in receipts of social housing supports).

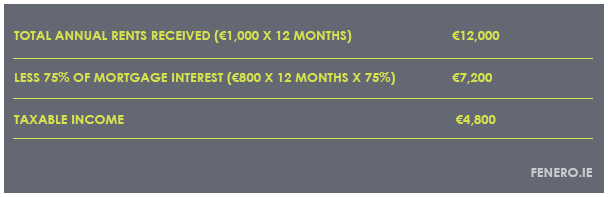

BY WAY OF ILLUSTRATION:

John is renting out his home. He receives €1,000 per month in rent from his tenant. His mortgage repayment is €1,200 per month, of which €800 relates to interest.

Assuming that John had absolutely no other expenses in the year, John’s taxable income would be worked out as follows:

Therefore even though John has a shortfall of €200 per month between what is receiving in rents and what is paying out on his mortgage, he will still be taxed on €4,800 at the end of the year.

In some cases PRSI is also payable on rental profits. Since 1 January 2013 PRSI is payable on rental profits if you also have self-employed income. And from 1 January 2014, all “chargeable persons” pay PRSI on rental income, thereby bringing some PAYE employees into the scope of this tax. Due to this extra PRSI charge it is important to establish if you are considered to be a “chargeable person” (see definition in (1) above). If you are not a “chargeable person” you will avoid 4% PRSI on your rental income.

3. Preliminary tax

If you are a “chargeable person” you may be required to pay preliminary tax. Preliminary tax is essentially a payment on account towards your current year tax bill. This must be paid by 31 October each year. For example, you are required to make a payment on account towards your 2017 tax bill before 31 October 2017.

The only time you are not required to make a payment on account is in your first year. If you decide not to make a payment on account in your first year, you may have a “double” tax payment in the second year.

If you are not a “chargeable person” you are not required to pay preliminary tax.

THIS IS BEST EXPLAINED BY AN EXAMPLE:

John rented his property out for the first time in 2015. John decided not to make a payment on account for his 2015 tax bill during 2015. When 31 October 2016 came around, John submitted his income tax return for 2015 and paid his 2015 tax bill. However as it was now 2016 and John’s second year of renting out his property, on 31 October 2016 he was also required to make a payment on account for his 2016 income tax return. Therefore on 31 October 2016, John was required to pay his tax bill for 2015 and also to make a payment on account for his tax bill for 2016.

This is not an extra tax bill, as the tax for 2015 and 2016 were both always required to be paid. It is just a cash flow issue that you need to budget for.

If you do not pay preliminary tax when you are required to, you may be charged interest by Revenue for late payment of taxes.

4. You will lose the TRS relief on your mortgage repayments

Tax Relief at Source (TRS) is tax relief for the interest paid on a qualifying mortgage on your home. This is paid at source by your bank/mortgage provider, meaning your monthly repayment is automatically reduced by the amount of the tax relief. If you are currently in receipt of TRS, it is important to be aware that you are no longer entitled to receive this when you rent out your property. The effect of this will be to increase your monthly mortgage repayment so it is vital to ensure you account for this increase when working out the financial implications/benefits of renting out your home.

It is your responsibility to advise Revenue that you are no longer entitled to receive TRS. You can do this using a TRS4 Form (available on the Revenue website www.revenue.ie) or by contacting the TRS Helpline on 1890 46 36 26 or by emailing trsadmin@revenue.ie. If you do not notify Revenue, you will be liable to return the TRS received and may possibly be charged interest and penalties on top when they eventually become aware.

5. You must register with the PRTB

The Private Residential Tenancies Board (PRTB) is a government agency. The PRTB operates the national registration system for all private residential tenancies. When you rent out your property you are required to register with the PRTB within one calendar month of the tenancy commencing. A fee is payable for this registration. The fee increases for late registrations. In order to keep costs down, you must ensure this registration is submitted on time.

It is extremely important to be aware that if you not register with the PRTB, you will not be entitled to claim your mortgage interest as a tax deduction. As mortgage interest is by far the largest tax deduction for most people, failure to register with the PRTB will mean a substantially high tax bill. In the event of a Revenue Audit, you will be required to present your PRTB notice of registration.

In our illustrative example of John above, if all circumstances remained the same and the only difference was that John did not register with the PRTB, John’s taxable income would be a hefty €12,000 instead of €4,800.

6. You must obtain a BER certificate

From 1st January 2009 it has been compulsory to hold a BER certificate for all properties that you rent out. A BER certificate is essentially an energy label, similar to those found on electrical appliances. The purpose of this is to enable prospective tenants to take energy performance and energy costs into consideration when deciding what property to rent. When advertising your property for rent, the law states that you must include the BER rating details. Prospective tenants are entitled to request a copy of the BER certificate from you. More information can be found at SEAI websitehttp://www.seai.ie/Your_Building/BER/BER_FAQ/FAQ_BER/General/What-is-a-BER-.html

7. You will continue to be liable to the Local Property Tax

The Local Property Tax (LPT) is payable by property owners and not tenants. You are liable to the LPT on all properties that you own, even if you are not living in them. It is important to remember that this will be an ongoing cost even when you are no longer living in the property.

8. Your mortgage provider may need to be informed

Most mortgage agreements are arranged on the basis that the property is either your private home or an investment property and that you must let them know if this changes. You should check your loan agreement to see if there are any implications of changing the property status to an investment (i.e. rental) property. For example, if you would lose a tracker rate. Anecdotal evidence suggests that in general banks are not currently enforcing any rights they may have in this regard, but you should still do your homework. If you have any doubts as to the terms of your loan agreement, you should contact your mortgage provider or seek legal advice.

9. What to do if you rent out your home and move abroad

Although more people are once again starting to return home to Ireland after leaving during the financial crisis, a large number are still abroad. Many of these people are homeowners who decided to rent out their home either because they cannot afford to sell or because they wish to hold onto their home in the hope of returning in the future.

If you are a landlord living abroad, your tenant is legally required to withhold 20% of the rent and pay this over to Revenue. You obtain this 20% back from Revenue on submission of your annual income tax return. The 20% is first used to settle any tax bill that you may have and the balance is then refunded to you. Whilst this is not an extra cost, it is a cash flow implication that you need to factor in when considering your ability to meet your mortgage repayments.

The tenant is not required to deduct this 20% if you are using the services of a collection agent, resident in Ireland, who collect the rents on your behalf.

Further Useful Resources for First Time Landlords can be found at:

http://www.revenue.ie/en/tax/it/leaflets/it70.html Revenue’s Guide to Rental Income

www.prtb.ie The Private Residential Tenancies Board (A Government Agency)

www.irishlandlord.com An online resource created by landlords for landlords

www.ipoa.ie Irish Property Owners Association

www.threshold.ie Threshold, the National Housing Charity